Why Modern Risk Assessments Matter

Under CIRO requirements, advisors must collect and maintain accurate, up-to-date client information to support ongoing suitability determinations, including a client’s objectives, time horizon, and ability to take risk as circumstances change.

Advisors already understand the importance of risk assessments. What has changed is how those expectations need to be met in practice.

Traditional risk form workflows are often static. Forms are completed once, stored away, and revisited only during major reviews. This makes it difficult to compare how a client’s risk profile evolves over time or to account for significant life changes as they happen.

Modern risk assessments are designed to be accessible, flexible, and repeatable. When forms are easy for clients to complete and update, advisors gain a clearer picture of how risk tolerance shifts due to changes in income, family structure, health, or market conditions. Clients can proactively update their information instead of waiting for the next formal review.

This approach supports more accurate recommendations, stronger documentation, and advice that stays aligned with real-world client circumstances.

As Investopedia notes, “Advisors must determine the most suitable investments for each client”. A proper risk form supports that responsibility.

Key Takeaways

Before diving deeper, here’s what every advisor should know:

- Risk forms align client goals with suitable investment strategies

- Strong forms combine objective measures with behavioural insights

- Poorly designed forms introduce bias and incomplete documentation

- Risk profiles should evolve as clients’ lives change

- Digitized forms improve accuracy, efficiency, and client experience

Key Components of a Strong Risk Form

1. Client Goals

Every financial goal requires a certain level of risk and expected return. A well-designed risk form ensures clients’ investment expectations align with their comfort level and time horizon, reducing the likelihood of future dissatisfaction or reactive decision-making.

2. Objective Ability to Take Risk

A complete risk assessment considers both:

- Risk Attitude: How clients think and feel about risk

- Risk Capacity: Whether clients can financially withstand market volatility

Evaluating both provides a more accurate view of the level of risk a client can reasonably support.

3. Behavioural Risk Tolerance

Market volatility tests emotions as much as portfolios. Behavioural risk tolerance assesses whether clients can remain committed to their plan during periods of stress, uncertainty, or short-term losses. This insight is critical to building strategies clients can stick with over time.

Common Flaws in the KYC Process

While advisors know risk assessments are required, many traditional forms still fall short of capturing meaningful client insights.

Recent research from Canada’s Financial Wellness Lab and Ortec Finance shows that although firms are adapting to evolving suitability standards, only about 40 % currently incorporate goal feasibility into risk assessments. This reveals a widespread gap between compliance checklists and truly actionable profiles.

This highlights how many forms miss connecting risk profiles to real financial objectives, and it reflects deeper issues with conventional questionnaire design:

- Middle-Of-The-Road Responses: When presented with multiple scenarios, clients often default to a “just right” answer rather than their actual preference, which can distort risk profiles.

- Demand Characteristics: Clients sometimes answer based on what they think the advisor expects, rather than how they genuinely feel about risk or loss.

- Form Fatigue: Longer forms do not necessarily produce better insights. In many cases, they increase disengagement and reduce accuracy.

- Static and Isolated Snapshots: Traditional forms are often one‑off exercises that do not easily track changes in client perspectives over time or capture shifts caused by life events.

These flaws matter because clients’ responses are influenced by more than just their stated risk tolerance. Context, recent market events, and the way questions are presented can all sway answers, yet many traditional forms fail to account for these factors.

Poorly implemented designs often produce incomplete or misleading insights, leaving advisors with risk profiles that do not reflect how clients actually behave in real-world situations.

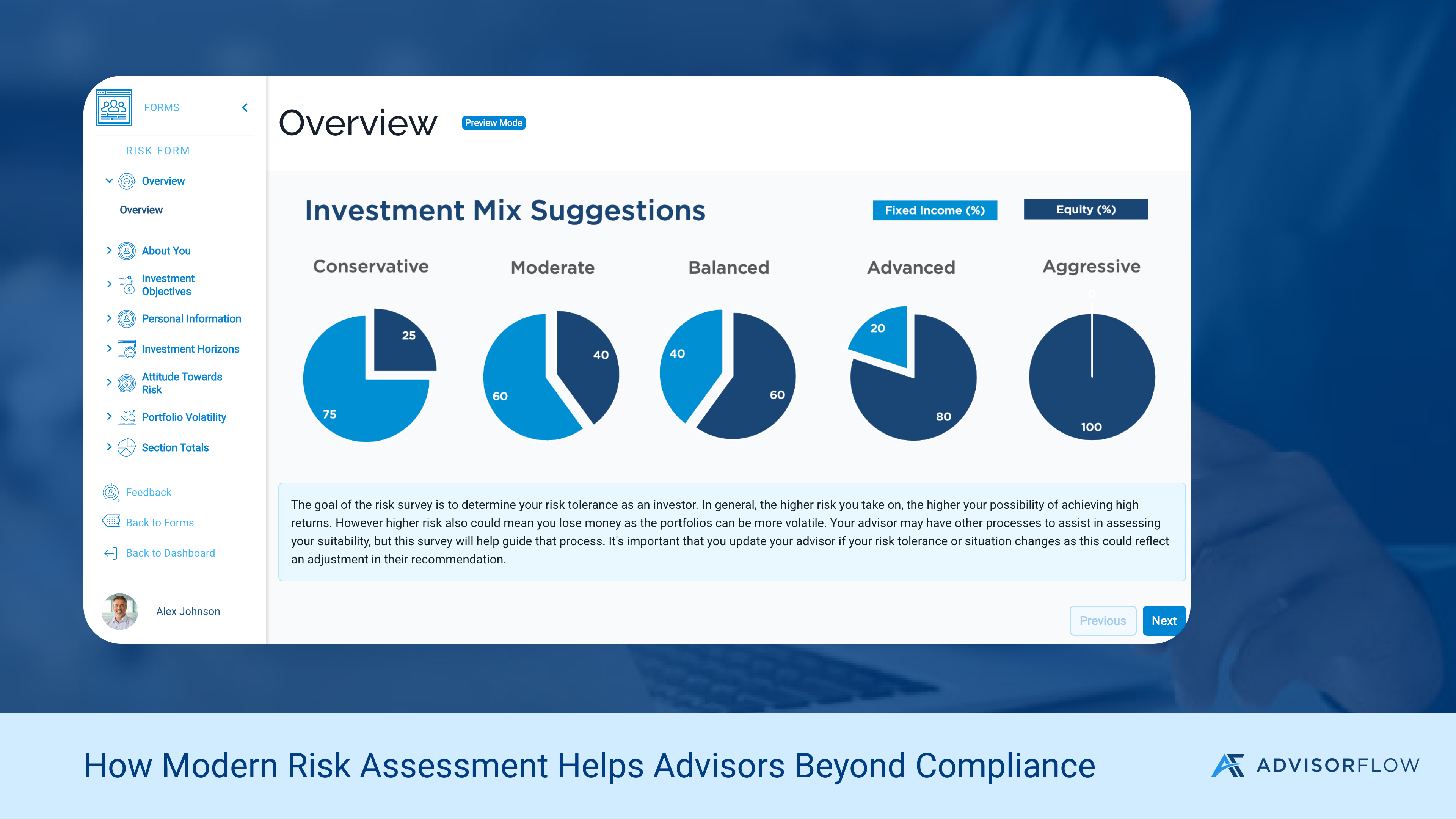

AdvisorFlow’s Digital Risk Form

AdvisorFlow’s digital risk form is designed to support a more complete, accurate, and client-friendly assessment process. It combines risk attitude, behavioural tolerance, and risk capacity within a single digital experience.

By making forms easier to complete and update, AdvisorFlow helps advisors reduce behavioural bias, capture more accurate insights, and maintain up-to-date documentation over time.

Benefits for Advisors Include:

- Faster, streamlined digital assessments

- Customizable questions aligned to firm workflows

- Easier updates as client circumstances change

- Clear KYC documentation supporting compliance

- Fewer missing or incomplete records

Beyond efficiency, digital risk forms improve consistency, create clearer audit trails, and help advisors spend less time on paperwork and more time on planning and client relationships.

Your Next Step

Understanding risk is not a one-time task. Regularly updated, well-designed forms keep your advice suitable, compliant, and aligned with what clients actually experience over time.

Explore how AdvisorFlow’s digital risk form can help you deliver a modern, efficient, and client-focused risk assessment.

🔗 Learn more about AdvisorFlow Risk Assessments